.jpg)

The architecture of a successful property investment relies as much on optimal capital structuring as it does on the physical asset itself. At the absolute centre of this structural framework lies the cost of debt, dictated primarily by buy-to-let mortgage rates. For property investors operating within the UK market, understanding the intricate mechanics of these rates is fundamentally essential. Borrowing costs do not merely represent an operational expense; they directly govern ongoing cash flow viability, yield preservation, and the long-term compounding of capital.

This comprehensive guide details the precise mechanisms of how buy-to-let mortgage rates are formulated, the macroeconomic and regulatory variables that influence institutional lender pricing, and the sophisticated quantitative methodologies that professional investors utilise. As a core component of broader finance, tax, and scaling strategies, mastering buy to let mortgage comparison enables investors to align their financing precisely with their overarching portfolio objectives.

The selection of a mortgage product is not merely a transactional requirement or a hurdle to property acquisition; it is a profound strategic decision. Securing the best buy to let mortgage rates determines how heavily a property can be safely leveraged, how well the investment can weather macroeconomic volatility, and ultimately, how efficiently the portfolio generates intergenerational wealth. Through a nuanced understanding of lender pricing models, investors can transition from passive rate-takers to strategic financial architects.

Executive Summary

For property investors, securing the most suitable buy-to-let mortgage is a critical strategic decision that dictates ongoing cash flow, long-term profitability, and overall portfolio growth. Navigating the complex landscape of mortgage pricing requires moving beyond simple headline rates to understand institutional risk modelling, corporate tax implications, and the true overall cost of debt. The following summary outlines the core mechanisms of buy-to-let mortgage rates and how professional investors evaluate their financing options:

- The Cost of Capital: Buy-to-let (BTL) mortgage rates are inherently higher than standard residential rates because lenders view them as a riskier investment. This pricing premium reflects the commercial nature of the loan, the dependency on third-party tenant income, and the strict regulatory capital requirements imposed on lenders by authorities like the Prudential Regulation Authority (PRA).

- Key Pricing Drivers: Mortgage pricing is heavily stratified based on institutional risk. The most significant factors influencing a rate include the Loan-to-Value (LTV) ratio, the complexity of the property, the borrower's legal structure, and whether the borrower is classified as a "portfolio landlord" (defined by the PRA as owning four or more mortgaged BTL properties).

- Corporate vs. Personal Ownership: Following tax changes that reduced mortgage interest relief for individuals, many investors now purchase properties through Limited Companies or Special Purpose Vehicles (SPVs). While SPV mortgage rates are typically marginally higher due to enhanced corporate underwriting requirements, the ability to offset 100% of the mortgage interest against corporation tax often results in superior net profitability for higher-rate taxpayers.

- The "Total Cost of Borrowing" Framework: Professional investors never select a mortgage based solely on the lowest headline interest rate. Instead, they calculate the true total borrowing cost over the fixed term by factoring in high percentage-based arrangement fees, valuation costs, legal disbursements, and the Annual Percentage Rate of Charge (APRC). An artificially low interest rate combined with a high capitalised fee is often more expensive overall than a higher rate with a standard flat fee.

- Macroeconomic Influences: Buy-to-let rates are dictated by broader financial markets. Variable and tracker rates move in tandem with the Bank of England Base Rate, while fixed-rate mortgages are priced according to wholesale "Swap Rates," which reflect the financial market's forward-looking forecast of the cost of money. Understanding these dynamics helps investors better anticipate rate changes and time their product selection.

How Buy-to-Let Mortgage Rates Work

Buy-to-let mortgage rates represent the institutional cost of capital charged by financial entities for lending against non-owner-occupied residential property. Unlike commercial real estate finance, which often involves highly bespoke pricing based on business operational metrics and subjective relationship banking, buy-to-let rates are generally productised. They are offered through highly structured, standardised matrices based on strictly defined risk parameters. Understanding how this interest is calculated and applied is the first step in mastering mortgage product comparison.

Mortgage Interest Rates Explained

At its fundamental core, a mortgage interest rate is the percentage of the outstanding principal balance that the lender charges annually for the provision of capital risk. In the context of the UK buy-to-let market, the overwhelming majority of investors strategically utilise interest-only structures rather than capital repayment models. To explore this vital structural difference further, refer to the dedicated guide on interest-only versus repayment mortgages.

Because the capital balance on an interest-only mortgage remains static throughout the lifetime of the loan (unless voluntary overpayments are made by the borrower), your monthly interest payment appears quite straightforward. However, behind the scenes, lenders actually calculate interest on a daily basis. They do this by taking your total outstanding loan balance, multiplying it by your annual interest rate, and then dividing that figure by 365 days in the year. This daily interest is then added up over the specific number of days in your billing month and charged to your account. Because the principal balance does not automatically diminish month-on-month, the absolute interest cost over the lifespan of the asset remains highly sensitive to the initial rate secured, placing immense strategic importance on precise product selection. Even a seemingly negligible variation of 25 basis points (0.25%) in the agreed buy to let mortgage rates can result in tens of thousands of pounds of wealth transfer from the investor to the lender over a holding period.

Annual Percentage Rates of Charge (APRC)

When reviewing and comparing mortgage products, investors will universally encounter the Annual Percentage Rate of Charge (APRC), a mandatory metric displayed alongside the headline rate. Regulatory bodies require lenders to publish the APRC to reflect the theoretical total cost of the mortgage over its entire lifetime.

The calculation of the APRC is based on the assumption that the borrower will remain with the same lender for the full standard term of the mortgage (often 25 years), transitioning from the initial introductory fixed or tracker rate onto the lender's far more expensive Standard Variable Rate (SVR) once the initial incentive period expires, and remaining there until the debt is cleared.

While the APRC provides a standardised regulatory benchmark designed to protect retail consumers from hidden fees, it is fundamentally misaligned with how professional property investors operate. Strategic investors rarely, if ever, allow a mortgage to revert to the punitive SVR. Instead, they actively manage their debt facilities, refinancing the asset at the end of the initial product term to secure a new preferential rate or to extract newly created equity. For an in-depth understanding of these refinancing mechanics, consult the buy-to-let remortgaging guide. Consequently, sophisticated mortgage product comparison relies less on the mandated APRC and almost entirely on calculating the true "total borrowing cost" strictly over the specific introductory period.

Fixed, Tracker, and Variable Structures

The primary categorical division in buy-to-let mortgage rates lies in the interest rate structure, which dictates how the rate behaves over time:

- Fixed-Rate Mortgages: The interest rate is contractually locked for a predetermined periodmost commonly two, three, or five years, though longer tenures of up to ten years exist in the market. This structure provides absolute payment certainty regardless of broader economic fluctuations.

- Tracker Mortgages: The interest rate tracks a nominated external benchmark - usually the Bank of England Base Rate plus a set percentage margin (e.g., Base Rate + 1.50%). The rate will mechanically fluctuate in direct tandem with macroeconomic monetary policy decisions.

- Variable-Rate Mortgages: These rates, including discount variable products, fluctuate at the discretion of the individual lender, typically reflecting the lender's internal cost of funds, competitive positioning, and broader market conditions.

The practical implications of these structures for investors are profound. The pricing differentials across these product types represent the financial market's collective forecast of future economic conditions. By selecting a fixed rate buy to let mortgage, the investor is essentially purchasing an insurance policy against rising rates from the lender. By selecting a tracker buy to let mortgage, the investor retains the interest rate risk, capitalising on potential future rate cuts but exposing their cash flow to the danger of rate hikes.

Why Buy-to-Let Mortgage Rates Are Higher Than Residential Rates

A ubiquitous observation among property investors is the persistent pricing premium attached to buy-to-let mortgages compared to their residential, owner-occupier counterparts. This premium, which historically ranges between 1% and 3% above standard residential pricing, is not an arbitrary penalty levied against landlords; it is the direct mathematical output of institutional credit risk modelling and highly stringent regulatory capital requirements. Further distinctions between the structural mechanics of the two lending types can be explored in the buy-to-let vs residential mortgage comparison.

Investment Lending vs Owner-Occupier Lending

From a fundamental credit risk perspective, a residential mortgage is serviced by an individual's personal, diversified earned income, and the physical property serves as their primary shelter. The behavioural motivation for a borrower to maintain payments and avoid losing their primary home is exceptionally high, resulting in historically low default rates.

In stark contrast, a buy-to-let mortgage is underwritten as a commercial transaction. The asset is purely an investment vehicle, and the primary source of debt service is the rental income generated by third-party tenants. This completely alters the risk profile for the lending institution.

Lender Risk Considerations and Rental Dependency

Lenders classify buy-to-let lending as inherently higher risk due to its acute exposure to external, uncontrollable variables. The property investor has limited control over tenant behaviour, unexpected void periods, and sudden macroeconomic shifts in local rental demand. If a property sits vacant due to extensive necessary repairs or a lack of tenant demand, the primary revenue stream servicing the debt is entirely severed.

Furthermore, during periods of severe economic distress, an investor facing broad financial hardship will invariably default on an investment property long before defaulting on their primary residence. To compensate for this elevated Probability of Default (PD) and the associated Loss Given Default (LGD), lenders must apply a risk premium to the interest rate to ensure the portfolio remains profitable.

Regulatory Frameworks and Lender Capital Requirements

The most structurally significant reason for the buy-to-let rate premium lies deep within global banking regulations, specifically the capital adequacy requirements enforced by the Prudential Regulation Authority (PRA) in the UK. Under complex banking regulations such as the transition toward the Basel 3.1 standards, financial institutions cannot simply lend out all the money they hold. They must hold a specific percentage of high-quality capital in reserve against the loans they issue to ensure systemic stability in the event of a market crash.

The amount of capital a bank is legally mandated to hold in reserve is dictated by the "risk weight" assigned to the specific asset class. Because global regulatory bodies view buy-to-let mortgages as higher-risk exposures than standard residential mortgages, they assign a significantly higher Risk-Weighted Asset (RWA) percentage to them.

For instance, under proposed Basel 3.1 implementations, the PRA notes that capital requirements for banks will increase, particularly impacting mid-tier institutions that originate high volumes of specialist buy-to-let loans. If a lender is forced by the regulator to lock away more of its expensive tier-one capital to issue a buy-to-let mortgage, the lender's internal Return on Equity (ROE) diminishes. To restore their profit margins to acceptable shareholder levels, banks have no choice but to pass the cost of this capital requirement directly to the property investor in the form of higher interest rates. This regulatory capital charge is the primary driver of the spread between residential and buy-to-let mortgage deals.

What Affects Buy-to-Let Mortgage Rates

Beyond the macroeconomic baseline set by central banks, the specific interest rate offered to an individual investor on a specific property is determined by a confluence of transaction-specific and borrower-specific variables. Lenders utilise complex underwriting algorithms that adjust pricing dynamically based on layered risk factors.

It is vital to note that this section discusses these factors purely in terms of how they influence the pricing of the mortgage rate. For comprehensive details on how these factors affect your ability to qualify for the loan or the total amount you can borrow, please refer to our guide on how much you can borrow on a buy-to-let mortgage.

Loan-to-Value (LTV)

The Loan-to-Value ratio is arguably the most potent single determinant of a mortgage product's interest rate. LTV represents the size of the loan relative to the property's appraised valuation. Lenders heavily stratify their interest rates across standard LTV bracketstypically 60%, 70%, 75%, and 80%.

The selection of a mortgage product is not merely a transactional requirement or a hurdle to property acquisition; it is a profound strategic decision.

The most critical and devastating error an investor can make when selecting a buy-to-let mortgage is to execute a linear comparison based solely on the headline interest rate.

As the LTV increases, the investor's equity buffer inherently shrinks. In the event of a severe default leading to repossession and a forced distressed sale, a higher LTV significantly increases the statistical risk that the lender will not recoup their principal if regional property prices have depreciated. Consequently, a 60% LTV product will always feature a vastly more competitive rate than a 75% LTV product, directly reflecting the lower loss severity profile. For a detailed breakdown of how capital input thresholds and deposits are structured, refer to the buy-to-let mortgage deposit requirements article.

Property Type and Asset Complexity

The physical characteristics and operational nature of the underlying real estate heavily influence mortgage pricing. Standard "vanilla" residential units, such as modern terraced houses or purpose-built flats, attract the most competitive buy to let rates because they are highly liquid; if the lender must repossess the property, it can be easily sold on the open residential market to owner-occupiers.

Conversely, complex assets such as Houses in Multiple Occupation (HMOs), Multi-Unit Freehold Blocks (MUFBs), or properties constructed from non-standard materials present higher operational risks, lower secondary market liquidity, and more complex valuation parameters. The buyer pool for an eight-bedroom HMO is restricted almost entirely to other investors. Lenders offset the illiquidity, higher management risks, and bespoke underwriting required for these assets by applying higher interest rates.

Borrower Profile: Personal vs Corporate Ownership

The legal structure utilised by the investor to acquire the property dictates which specific segment of a lender's product range they can access. Corporate borrowers, for example, will need to review specific company buy to let mortgage rates. Mortgages acquired through a Special Purpose Vehicle (SPV) or a Trading Limited Company typically carry slightly higher interest rates than personal name buy-to-let mortgages.

The pricing differential arises from the additional legal complexities of lending to a corporate entity, the enhanced underwriting requirements to assess company accounts, and the registration of corporate floating charges. The specific nuances of this pricing differential are explored in depth in Section 5 of this report.

Portfolio Landlord Status

Under PRA guidelines introduced in 2017, an investor possessing four or more mortgaged buy-to-let properties is legally classified as a "portfolio landlord". This classification triggers mandatory, enhanced regulatory scrutiny. Lenders are required to stress-test the entire background portfolio to ensure that underperforming assets elsewhere in the investor's wider estate do not threaten the viability of the new loan application.

Because portfolio underwriting is highly resource-intensiverequiring skilled underwriters to analyse complex business plans, cash flow forecasts, and extensive asset schedulesenders often price portfolio mortgage products slightly higher to absorb these increased operational costs. Furthermore, some high-street lenders withdraw entirely at the portfolio threshold, leaving the investor reliant on specialist commercial lenders whose baseline cost of funds is inherently higher. Further rules surrounding this classification are detailed in the portfolio landlord rules guide.

Lender Appetite and Market Conditions

Mortgage pricing is not always a pure, mathematical reflection of asset risk; it is frequently utilised as a blunt macroeconomic tool to modulate lender supply and borrower demand. If a lender holds a surplus of wholesale capital allocated for buy-to-let lending, they will aggressively cut interest rates to capture market share and deploy those funds efficiently.

Conversely, if a lender is rapidly approaching its internal lending limits, or wishes to slow down application volumes to protect their customer service levels and underwriter bandwidth, they will implement "defensive pricing" - artificially increasing their current buy to let mortgage rates to deter new applications without having to formally withdraw their products from the market entirely.

Fixed vs Tracker vs Variable Buy-to-Let Mortgages

Selecting the optimal interest rate structure requires a highly strategic balancing of an investor's risk tolerance, portfolio budgeting constraints, and their macroeconomic forecasting. Each structure offers distinct operational advantages and inherent vulnerabilities.

The Strategic Role of Fixed-Rate Mortgages

A variable rate buy to let mortgage fluctuates at the lender's discretion, often loosely following the base rate but retaining the right to move independently. Tracker mortgages, on the other hand, are contractually pegged to an external economic index, most commonly the Bank of England Base Rate, ensuring transparency.

Advantages:

- Absolute Budgeting Certainty: Yields and cash flows can be projected with mathematical certainty over the fixed term, allowing for precise capital allocation and reinvestment planning.

- Protection from Inflationary Shocks: If central banks hike base rates aggressively to combat spiralling inflation, the investor’s debt servicing costs are entirely unaffected until the fixed period expires.

- Favourable Stress Testing and Maximum Leverage: Due to PRA rules, five-year fixed-rate products are often assessed by lenders using the actual "pay rate" rather than a heavily inflated notional stress rate. This regulatory quirk allows investors to access significantly higher borrowing capacities than they would be granted on a two-year fix or a variable product. To understand the specific metrics used by lenders in this scenario, review buy-to-let affordability stress testing.

Disadvantages:

- Early Repayment Charges (ERCs): The price of certainty is a lack of flexibility. Exiting the mortgage, selling the property, or attempting to refinance before the fixed term ends typically incurs punitive financial penalties (often a percentage of the outstanding loan).

- Rate Lock-In Risk: If broader market interest rates plummet, the investor remains contractually locked into the higher rate, potentially missing out on drastically improved cash flow and higher yields.

The Strategic Role of Tracker and Variable Mortgages

Tracker buy to let mortgages are contractually pegged to an external economic index, most commonly the Bank of England Base Rate, ensuring transparency. Variable rate buy to let mortgages fluctuate at the lender's discretion, often loosely following the base rate but retaining the right to move independently.

Advantages:

- Downside Participation: If economic conditions deteriorate and central banks aggressively cut interest rates to stimulate the economy, tracker rates automatically adjust downward. This instantly reduces the investor's monthly mortgage payment, expanding their profit margins without requiring any refinancing action.

- Unmatched Flexibility and Liquidity: Many tracker and variable products feature minimal or no Early Repayment Charges. This is a profound advantage for active investors undertaking aggressive portfolio recycling, planning a near-term sale of the asset, or executing a "Buy, Refurbish, Refinance" (BRR) strategy where the capital needs to be unencumbered and extracted quickly.

Disadvantages:

- Cash Flow Instability and Margin Compression: Monthly payments can rise sharply and without warning. If rental increments cannot keep pace with rising debt costs, the profitability of the asset can be rapidly eroded, potentially leading to negative cash flow.

- Restrictive Stress Testing: Because variable rates expose the lender to immediate default risk if rates spike, the affordability calculations applied to these products are extremely punitive. Lenders will stress the application at a significantly higher notional rate (e.g, pay rate plus 2% or 3%), substantially reducing the maximum loan amount available to the investor.

Limited Company and SPV Mortgage Rates

The divergence between personal and corporate mortgage rates is a critical consideration for modern investors. Historically, the vast majority of buy-to-let properties were purchased in personal names. However, the introduction of Section 24 of the Finance (No. 2) Act 2015, which restricted the ability of individual landlords to deduct mortgage interest from rental income for tax purposes, drove a massive structural shift toward corporate ownership. For a comprehensive examination of corporate structures, refer to the limited company buy-to-let guide.

Corporate Legal Frameworks and Underwriting Differences

When an investor applies for ltd company buy to let mortgage rates, usually via a Special Purpose Vehicle (SPV), the lender is providing debt to a distinct, ring-fenced legal entity. Although the human directors provide Personal Guarantees (PGs) to underwrite the loan, the lender must interact with complex corporate insolvency law in the event of a default.

Lenders mitigate this structural complexity by requiring a floating charge or debenture over the company's assets, ensuring they rank as a preferential secured creditor. The slightly elevated interest rates applied to SPV mortgages cover the enhanced legal underwriting costs, the ongoing risk monitoring of corporate filings at Companies House, and the capital premiums associated with commercial-grade risk.

Common Misconceptions Regarding SPV Rates

A highly prevalent misconception among newer investors is that an SPV structure entirely shields the individual from affordability scrutiny. In reality, the lender underwriting process is inherently hybrid; lenders assess both the corporate entity's financial viability (primarily the rental coverage of the specific asset) and the individual directors' background creditworthiness and experience.

Another frequent misconception is that the marginally higher mortgage rate on an SPV nullifies its celebrated tax benefits. While SPV mortgage rates may be 20 to 50 basis points higher than an equivalent personal mortgage, the reality of the buy-to-let tax system often overrides this. The ability to offset 100% of the mortgage interest as a direct business expense against corporation tax, compared to the highly restrictive 20% tax credit available to higher-rate taxpayers holding properties personally usually results in a vastly superior net profit margin for the SPV structure, entirely eclipsing the slightly higher cost of debt.

How Professional Investors Compare Mortgage Deals

The most critical and devastating error an investor can make when selecting a buy-to-let mortgage is to execute a linear comparison based solely on the headline interest rate. The advertised rate is merely one component of a heavily structured, multifaceted financial product. To accurately compare competing buy to let mortgage deals, sophisticated investors entirely discard the headline rate as a standalone metric and instead utilise a comprehensive "Total Cost of Borrowing" analytical framework, ensuring all peripheral capital drains and incentives are accounted for over the intended lifecycle of the loan.

Deconstructing the Total Borrowing Cost

To compare buy to let mortgage rates effectively, professional investors construct a cash flow model that seamlessly integrates the interest rate with the associated setup and exit fees. The constituent elements of this true cost model include:

- Product / Arrangement Fees: These are the primary fees charged by the lender for accessing the specific interest rate. Crucially, in the buy-to-let sector, these fees have evolved aggressively from flat monetary amounts (e.g, £1,495) to percentage-based models (e.g., 2%, 5%, or even 7% of the total loan amount). An exceptionally low headline rate is almost universally subsidised by an exorbitant percentage fee.

- Valuation Fees: The cost of the surveyor physically assessing the asset to confirm its value and rental capability. Some products include free valuations as a lender incentive, which can save hundreds of pounds.

- Legal and Disbursement Fees: The conveyancing costs associated with registering the mortgage charge. Again, some lenders offer "free legals" or a cashback alternative to offset these costs.

- Cashback Incentives: A direct capital sum paid by the lender to the borrower upon completion, which effectively acts as a rebate against the initial setup costs, improving day-one liquidity.

- Early Repayment Charges (ERCs): The penalties applied if the mortgage is cleared before the fixed term expires. Investors planning future liquidity events must carefully model the ERC decay curve to assess the true cost of flexibility.

The Low Rate vs High Fee Paradigm

The recent proliferation of high-fee, low-rate buy-to-let mortgages is a direct institutional response to regulatory stress testing. Because lenders assess the maximum loan amount based primarily on the headline "pay rate," a lower interest rate allows the investor to pass the stress test and borrow significantly more capital. To offer that artificially low rate while preserving their internal profit margin, lenders dramatically increase the arrangement fee, which is typically added to the loan balance rather than paid upfront from the investor's cash reserves.

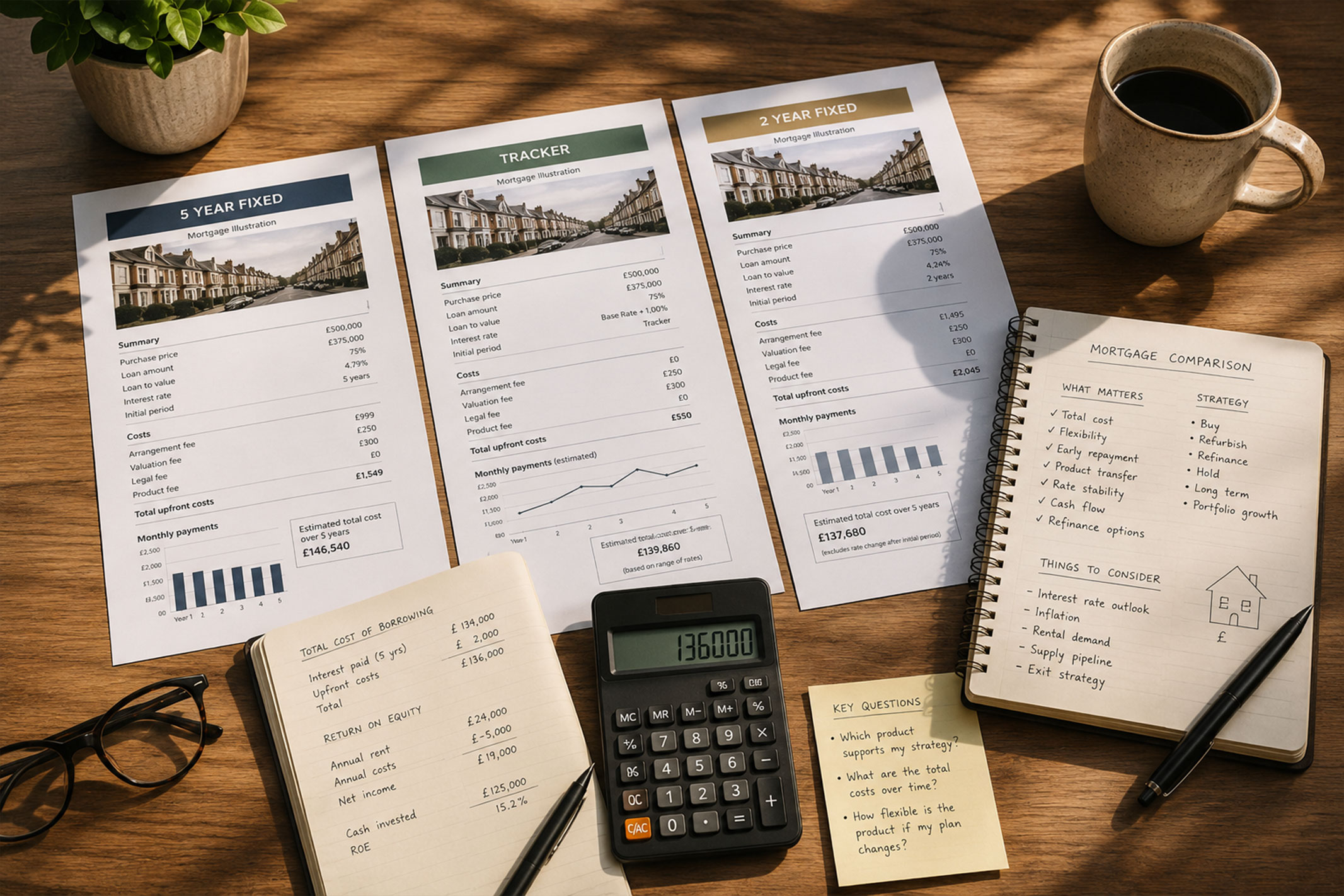

This dynamic creates a highly complex analytical scenario. Finding the best buy to let mortgage deals requires looking at the total quantum of debt over the fixed period. Consider an investor seeking a £200,000 buy-to-let mortgage on a five-year fixed term. They are presented with two seemingly distinct options:

- Option A: 4.25% Interest Rate with a 5% Arrangement Fee (£10,000 fee)

- Option B: 5.50% Interest Rate with a Flat Arrangement Fee (£1,995 fee)

At a superficial glance, Option A appears vastly superior due to the much lower interest rate, promising better monthly cash flow. However, a total cost analysis over the 60-month (5-year) fixed period reveals a nuanced reality.

In this specific £200,000 scenario, Option A remains the cheaper product overall, saving the investor approximately £2,918 over the five-year term, while also providing superior monthly cash flow.

However, this advantage is not static; it changes violently depending on the loan size. Let us run the exact same calculation for a highly leveraged asset requiring a £500,000 loan.

- Under Option A (the 4.25% low rate with a 5% fee), the capitalised arrangement fee balloons to £25,000, creating a gross loan balance of £525,000. The monthly interest payment is £1,859.38, bringing the total true cost (interest plus fee) over 60 months to £136,562.50.

- Under Option B (the 5.50% high rate with a flat £1,995 fee), the gross loan balance is £501,995. The monthly payment is £2,300.81, bringing the total true cost over 60 months to £140,043.60.

Even at £500,000, the 5% fee model narrowly wins out over the 5-year term. But if the investor sells in year three, paying an ERC, the heavy £25,000 capitalised fee of Option A makes it a catastrophic financial decision compared to Option B. As the loan size increases, the heavy capital drag of percentage-based arrangement fees can entirely negate the monthly cash flow savings generated by the lower interest rate. Investors must continuously model their precise loan quantum to determine where the mathematical threshold of profitability lies.

Furthermore, investors must account for the compounding effect. When an arrangement fee is added to the loan balance, the investor pays interest on the fee itself for the entirety of the mortgage term.

Evaluating Flexibility and Exit Costs

Professional comparison extends far beyond initial term costs to encompass future liquidity and structural flexibility. Two competing mortgage products may yield identical total borrowing costs over a five-year term, but one may feature an Early Repayment Charge that decays rapidly year-on-year (e.g, 5% in year one, dropping to 4%, 3%, 2%, 1%), while the other retains a punitive flat 5% ERC until the final month of the fifth year.

For an investor whose broader portfolio business plan may require the liquidation of the asset in year four to fund a much larger commercial acquisition, the product with the tapering ERC represents a vastly superior strategic choice, despite identical headline pricing metrics. Mortgage flexibility is a tangible asset that carries an intrinsic financial value.

How Mortgage Rates Impact Investment Returns

Mortgage selection is fundamentally an exercise in protecting and optimising the financial performance of the underlying real estate asset. The cost of debt acts as a direct, unyielding counterweight to the property's gross yield; the wider the spread between the two, the more profitable the investment.

Cash Flow and Profitability

Positive, reliable cash flow is the operational lifeblood of a property portfolio, ensuring that the asset can autonomously sustain its operational costs, ongoing maintenance requirements, and unforeseen void periods without requiring emergency capital injections from the investor's personal reserves. Because the monthly mortgage payment is almost universally the single largest expenditure line item, a variation of even 50 basis points (0.50%) in the interest rate can dictate whether an asset generates a meaningful monthly surplus or merely breaks even.

Rental Yields and Return on Equity (ROE)

The interplay between financial leverage and interest rates directly dictates the investor's Return on Equity (ROE). Leverage allows an investor to control a high-value, appreciating asset using only a fraction of their own capital (the deposit).

Consider a property purchased for £200,000, generating a stable £1,200 per month in rent (£14,400 annually).

- If purchased entirely with cash, the gross yield is 7.2%, and the Return on Equity is exactly 7.2%.

- If purchased using a 75% LTV mortgage (£150,000 loan, £50,000 deposit), the investor leverages their capital to amplify returns.

If the secured mortgage rate is highly competitive at 4.00%, the annual interest cost is £6,000. The net rent (before other operational costs for simplicity) is £8,400. Measured against the £50,000 initial deposit, the Return on Equity jumps to a highly attractive 16.8%.

If the secured mortgage rate rises to 6.00% due to poor product selection, the annual interest cost balloons to £9,000. The net rent drops to £5,400, and the Return on Equity plummets to 10.8%.

This stark contrast demonstrates exactly how sensitive investment velocity is to mortgage pricing. Capital compounds much faster when debt costs are ruthlessly minimised, allowing the investor to extract and redeploy surplus cash into subsequent property acquisitions.

Refinancing Flexibility and Long-Term Portfolio Growth

The choice of mortgage product also intrinsically impacts future portfolio growth capacity. A long-term fixed rate provides a highly stable foundation, but it severely limits the investor's ability to extract capital via refinancing if the property experiences rapid capital appreciation. An investor who locks into a rigid five-year fixed rate and successfully executes a high-value refurbishment project in year one will find their newly generated equity trapped behind punitive Early Repayment Charges for four long years. Consequently, the optimal mortgage rate must be aligned not just with current cash flow needs, but with the specific value-add timeline of the overarching business plan.

Portfolio projection tool

Current Market Conditions and Macro Dynamics

Monitoring current buy to let mortgage rates does not exist in a vacuum; it is the ultimate downstream output of a highly complex, interconnected global financial system. Understanding the macroeconomic variables that push rates up or down allows investors to anticipate market shifts, rather than merely reacting to them, enabling them to time their financing decisions effectively.

The Influence of the Bank of England Base Rate

The Bank of England's Monetary Policy Committee (MPC) sets the official Bank Rate to manage the trajectory of inflation and steer the wider UK economy. This base rate acts as the foundational gravitational pull for all domestic borrowing. Tracker and variable buy-to-let mortgages are inherently and directly tethered to this rate. When the central bank hikes the base rate to suppress consumer spending and cool inflation, variable borrowing costs for landlords rise immediately; when they cut the rate to stimulate economic growth, variable costs mechanically fall.

Swap Rates and the Pricing of Fixed Mortgages

While the base rate dictates variable products, fixed-rate mortgages are priced based on the wholesale financial markets, specifically "Swap Rates".

An interest rate swap is a complex derivative contract used by financial institutions to manage their own risk. In a simplified context, non-bank lenders and high-street banks use swaps to trade the unpredictable, floating interest rates of the future for a guaranteed, fixed cost of money today. The most relevant benchmark for these swaps in the UK is the Sterling Overnight Index Average (SONIA).

Swap rates are essentially the financial market's collective, aggregated prediction of where the Bank of England base rate will be over a set period (e.g., two, three, or five years into the future).

- If global financial markets anticipate that inflation will persist and central banks will be forced to raise rates in the future, Swap Rates will rise aggressively today. The lenders' wholesale cost of securing fixed funding increases, and they instantly reprice their retail fixed-rate buy-to-let mortgages upwards to protect their margins.

- Conversely, if markets anticipate an impending recession and aggressive future rate cuts, Swap Rates will fall sharply, leading to cheaper fixed-rate mortgages being offered to investors immediately, long before the Bank of England acts.

Because Swap Rates are forward-looking mechanisms, fixed buy to let mortgage rates often move weeks or even months before the Bank of England actually makes a formal base rate decision. Astute investors monitoring Swap Rate trends can often lock in products before lenders adjust their retail pricing matrices.

Economic Cycles and Lender Competition

In a stable macroeconomic environment, the sheer density and maturity of the UK mortgage market, monitored by trade associations like UK Finance, forces lenders to compete fiercely for market share. This intense competition compresses institutional profit margins, driving interest rates down and stimulating the introduction of borrower-friendly incentives like free valuations, scaled cashback, and reduced legal fees. However, during economic downturns or periods of high systemic stress, lender risk appetite retracts rapidly. Capital becomes scarce, underwriting criteria tighten significantly, and rates are adjusted upwards to reflect the deteriorating macroeconomic environment and the heightened statistical probability of borrower defaults.

Common Investor Mistakes in Product Selection

Because mortgage pricing can be confusing and securing finance is stressful, both new and highly experienced investors often make predictable mistakes. By identifying these common traps, you can optimise your decision-making process.

Over-Fixating on the Headline Rate

The most ubiquitous and damaging mistake is treating the lowest advertised interest rate as the optimal product. As demonstrated in the total cost analysis earlier in this report, an artificially low rate subsidised by a colossal percentage-based arrangement fee can strip thousands of pounds of hard-earned equity from the investment. A borrower fixated purely on the psychological victory of securing a rate beginning with a "3" rather than a "4" may inadvertently sign a structurally far more expensive contract.

Ignoring the Implications of Early Repayment Charges (ERCs)

Property investment requires significant operational agility. Locking a property into a five-year fixed-rate mortgage simply because the initial rate is slightly cheaper than a two-year fix, without rigorously accounting for the business plan, is a critical failure. If the investor decides to sell the asset or restructure the portfolio in year three to capitalise on a new opportunity, the subsequent ERCwhich can often total tens of thousands of poundswnstantly vaporise years of accumulated rental profit. Future flexibility must be priced into the initial decision.

Focusing on Affordability Over Suitability

Due to the punitive mechanics of the Interest Coverage Ratio (ICR) stress tests, investors are often highly incentivised to choose a five-year fixed product, as lenders test the affordability at the lower "pay rate" rather than a higher notional rate, thereby releasing more capital. While using a five-year fix to leverage higher borrowing is a mathematically valid strategy, it becomes a severe mistake when an investor accepts a five-year lock-in solely to pass an affordability test, even when their underlying business strategy requires a near-term exit or refinance. The tail of mortgage qualification should never wag the dog of investment strategy.

Neglecting to Compound Capitalised Fees

When arrangement, valuation, and broker fees are added to the total mortgage balance rather than paid upfront from cash reserves, the investor mechanically pays interest on those fees for the duration of the loan. Adding a £5,000 fee to a 5.00% mortgage over a 25-year term does not cost £5,000; the compounded interest effectively doubles the true cost of that fee over the asset's lifespan. Investors failing to model this capital drain artificially inflate the performance metrics of their portfolio and compromise their long-term equity growth.

Conclusion

Buy-to-let mortgage rates represent far more than a simple percentage cost applied to a loan; they are highly engineered financial instruments that respond continuously to macroeconomic forces, regulatory capital requirements, and institutional systemic risk assessments. For the property investor, the interest rate dictates the fundamental viability, the cash flow profile, and the compounding velocity of the underlying real estate asset.

The most successful investors in the market do not view mortgage selection as a mere search for the lowest advertised rate. Instead, they operate with a comprehensive, mathematically rigorous understanding of the total cost of borrowing. They meticulously calculate how product fees, valuation costs, and legal disbursements interact with the interest mechanism over the intended lifecycle of the loan, ensuring that capital is not leaked unnecessarily to financial institutions.

Furthermore, these investors balance the mathematical cost of debt against the absolute necessity for structural flexibility, ensuring that Early Repayment Charges and fixed terms are perfectly synchronised with their specific value-add timelines and exit strategies. Ultimately, mastering the mechanics of buy-to-let mortgage rates enables investors to treat debt not as a passive burden or a necessary evil, but as a dynamic, highly tactical tool. By aligning sophisticated mortgage product selection with disciplined asset management, investors can insulate their portfolios from macroeconomic volatility, aggressively optimise their return on equity, and build highly resilient, cash-generative property enterprises.

Comparison of Buy-to-Let Interest Rate Structures

Feature

Fixed-Rate Buy-to-Let

Tracker Buy-to-Let

Variable Buy-to-Let

.png)

-v1.avif)

Get investor insights and early access to opportunities

Join our investor briefings for structured insights, market updates, and priority access to new deals.

No spam, just timely insights for investors We respect your privacy and never sell your data

Buy to let investment and rental yield calculator

Impact of Loan-to-Value (LTV) on Interest Rates

LTV Tier

Lender Risk Profile

Relative Interest Rate

Total Borrowing Cost Comparison - £200,000 Loan

Metric

Option A (Low Rate, High Fee)

Option B (High Rate, Flat Fee)

Case study

- Property Price:£300k

- Mkt Value at purchase:£320k

- Day one equity:£20,000

- Yield:6.8%

- ROCE:30.1%

.avif)