.jpg)

Buy-to-Let Interest Rates: Is the UK Housing Market a Coiled Spring?

The UK property market is currently being shaped by a tug-of-war between two powerful economic forces: rising wages and expensive debt.

Since the pandemic, wages have risen significantly, rents have surged, and the UK housing shortage has persisted. Yet house price growth has remained relatively subdued. For many, the missing piece of this puzzle may simply be the cost of borrowing.

For property investors and landlords, understanding the mechanics of buy to let interest rates is essential. We have moved from an era of ultra-cheap money into a "higher-for-longer" rate environment. This shift has undeniably changed the mathematics of property investment.

However, looking beneath the surface reveals a fascinating picture. Some of the purchasing power to drive the market forward may already exist. The question is when it will be unleashed.

This article explores why the UK housing market may currently contain significant latent demand, what higher mortgage rates mean for landlords, and what could happen to property values if interest rates finally begin to fall while incomes remain elevated.

Executive Summary

For readers short on time, the key arguments of this article are summarised below.

- The Affordability Paradox: Nominal wages have increased by roughly 24% since 2020, significantly increasing theoretical borrowing capacity. However, mortgage rates in the 5.5% range prevent buyers from passing stress tests and deploying this capital.

- Market Resilience: Despite the aggressive tightening of monetary policy, house prices have not crashed. Stability is being underpinned by low unemployment, the prevalence of fixed-rate mortgages, and a severe lack of new housing supply.

- Expanding Rental Yields: Squeezed by Section 24 taxes and the new Renters' Rights Act, amateur landlords are exiting the market. This constricted supply has pushed rental growth well above house price growth, improving yields for professional investors.

- The "Uncoiling" Scenario: If interest rates ease toward the 3.5% to 4.0% range, a typical household could gain over £130,000 in purchasing power without increasing their monthly payments, unlocking latent demand.

- The Contrarian Opportunity: Reduced market competition and lower transaction volumes offer well-capitalised investors a highly attractive window to negotiate favourable terms and acquire high-yielding assets before borrowing costs normalise.

The Affordability Paradox: More Borrowing Power, But Less Spending Power

The most defining, yet misunderstood, feature of the current property market is the affordability paradox.

To understand it, we must look at how much household incomes have grown since the pandemic. In April 2020, the median annual pay for full-time employees in the UK was £31,461. By early 2026, that figure had jumped to £39,039 according to the Office for National Statistics. That represents roughly a 24% increase in base salaries over a relatively short period.

While inflation has eroded some of these gains in real terms, nominal income remains highly relevant for mortgage affordability because lenders assess borrowers using gross salary multiples. In other words, even if households do not feel 24% richer, higher salaries can still materially increase borrowing capacity.

At the same time, mortgage lenders eager for business have expanded their income multiples. While 4.5x a borrower's salary used to be the strict upper limit, lenders like Nationwide now offer up to 6.0x income multiples for eligible buyers earning over £75,000, and some private banks go even higher for high-net-worth clients.

On paper, this means households can legally borrow significantly more money today than they could five years ago.

Imagine a professional couple earning £80,000 in 2020. At a standard 4.5x multiple, their maximum borrowing capacity was £360,000. Today, if their wages grew by 25% to £100,000, and they qualify for a 5.5x multiple, their new theoretical maximum loan is £550,000. They have gained almost £190,000 in theoretical purchasing power.

So, why haven't house prices surged to match this expanded capacity? Because the cost of servicing that debt has doubled.

Post-COVID wages have risen sharply, but higher mortgage rates have prevented that purchasing power from reaching the housing market.

Even though buyers are permitted to borrow larger sums, a mortgage rate of 5.5% means the monthly payments would consume an unsustainable portion of their take-home pay. Consequently, they fail the lender's monthly affordability stress tests. Importantly, these stress tests often assume mortgage rates above current market levels, further restricting how much buyers can borrow even when incomes have risen. The purchasing power exists on paper, but it cannot currently be deployed because the cost of debt remains too high.

In many ways, today's housing market resembles a dam. Wages, rents and borrowing capacity have all risen behind it, while higher interest rates act as the barrier preventing that demand from flowing into house prices.

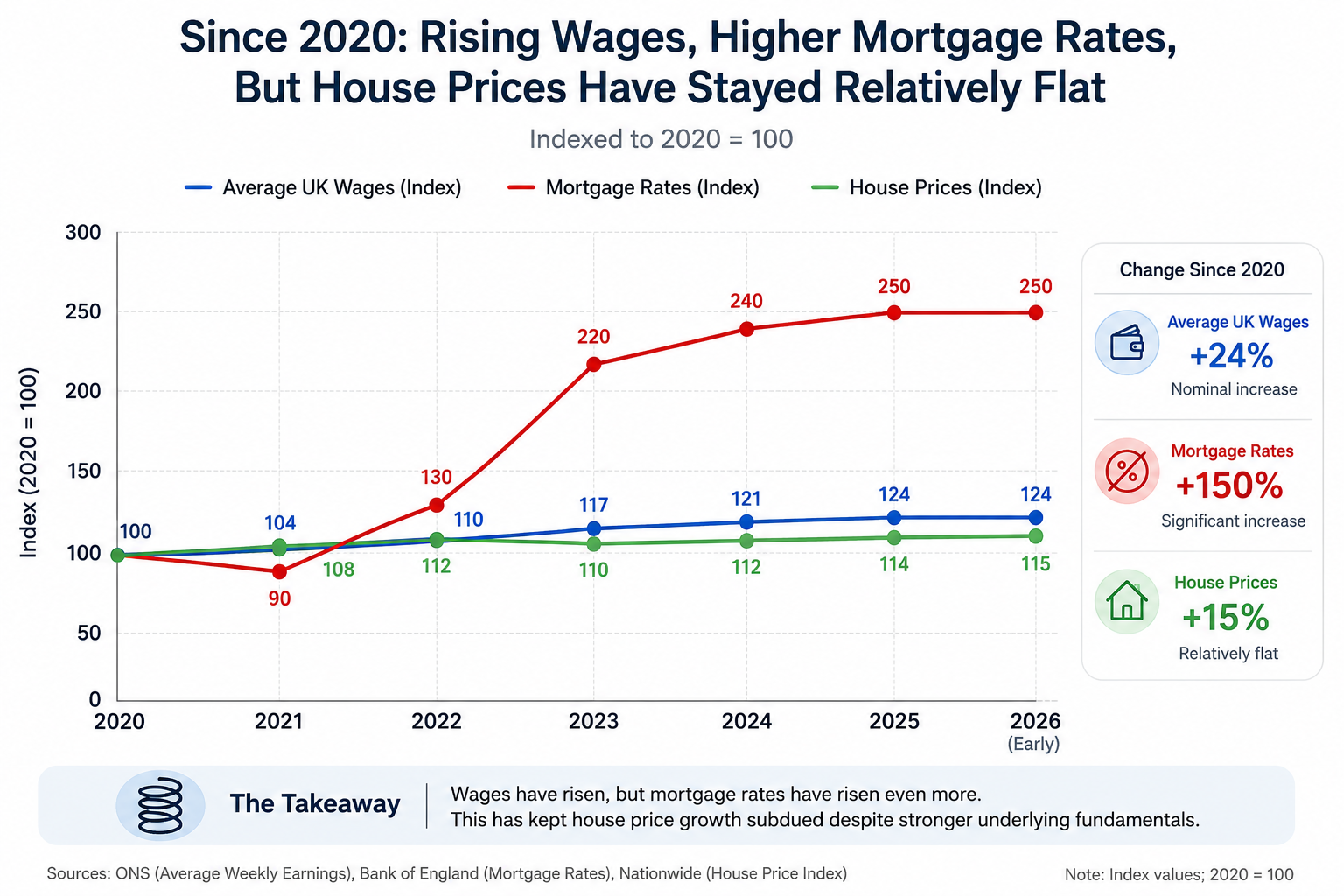

Since 2020: Wages and Mortgage Rates Have Risen Faster Than House Prices

The visual demonstrates a clear divergence: while both wages and the cost of debt have climbed aggressively, house prices have remained relatively flat, held in check by the affordability constraints of high interest rates.

Buy to let investment and rental yield calculator

Why Hasn't the Housing Market Fallen Further?

This brings us to one of the most interesting questions in the current market.

Mortgage rates rose from approximately 1-2% to 5-6%. Given the historical relationship between interest rates and house prices, a shock of this magnitude to the cost of borrowing might have caused a major correction, triggering widespread negative equity and a collapse in property values. Yet, house prices have remained remarkably resilient.

Despite the sharpest increase in mortgage rates in modern history, UK house prices have proved surprisingly robust. The reason may lie in a combination of stronger household finances, low unemployment, and a persistent shortage of homes.

There are four primary factors holding the market steady:

- Strong Wage Growth: As highlighted in the affordability paradox, a 24% increase in nominal wages has acted as a massive shock absorber. While higher mortgage rates have eroded spending power, higher salaries have largely offset the pain, allowing many homeowners to absorb the increased costs without defaulting.

- Low Unemployment: The housing market's resilience relies heavily on a robust labour market. While unemployment has ticked up slightly to 4.5% in early 2026, it remains low by historical standards. As long as people have jobs, they will prioritize their mortgage payments above almost all other discretionary spending.

- The Fixed-Rate Mortgage Structure: Unlike the 1980s and 1990s, when standard variable rates (SVRs) dominated the market, the modern UK mortgage market is heavily weighted toward two-year and five-year fixed-rate products. This means the pain of higher interest rates has not hit the market all at once; it is being digested slowly as legacy deals expire. This prevents a sudden, panicked wave of forced sellers.

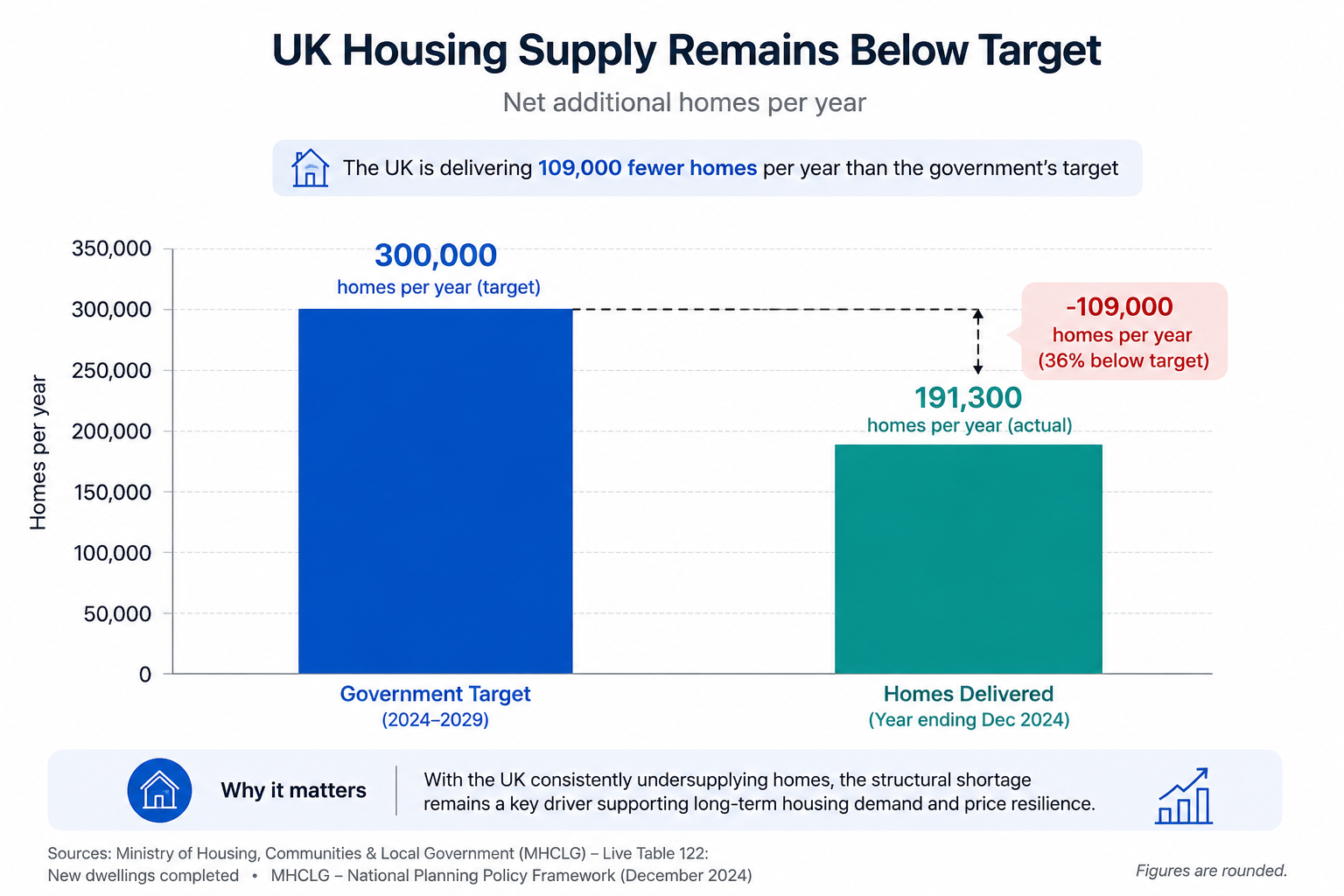

- Chronic Housing Shortages: The UK simply does not build enough homes. With the government consistently missing its target of 300,000 new homes per year, the sheer lack of physical inventory places a firm floor under prices. Current delivery estimates suggest only 191,300 net additional homes were delivered in the 12 months leading up to March 2026.

UK Housing Supply Remains Below Target

This persistent shortfall in housing delivery continues to place a firm floor under property prices.

While higher income multiples have improved borrowing capacity at the margin, the bigger drivers of market resilience remain wage growth, low unemployment, chronic housing shortages and the prevalence of fixed-rate mortgages.

Is This Time Different?

When observing the current stagnation, it is tempting to look back at the UK housing crashes of the early 1990s or the 2008 Global Financial Crisis. However, context is crucial.

Previous housing downturns in the UK were often accompanied by rapidly rising unemployment, a surge in forced selling, and structurally weaker household finances. Today's market looks different.

During the early 1990s crash, the effective interest rate on mortgage debt hit double digits, and mortgage payments consumed an unprecedented 27% of a buyer's gross income. Today, the stress is managed. While no cycle is identical, several structural features of today's market differ materially from previous downturns. Wage growth has been strong, unemployment remains relatively low, lending criteria have been vastly more responsible since 2014, and housing supply continues to drastically lag demand.

The UK housing market may not be broken, it may simply be waiting for cheaper debt.

The UK housing market may currently resemble a coiled spring: wages have risen, rents have surged and supply remains constrained - but higher mortgage rates continue to suppress demand.

How Interest Rates Affect Buy-to-Let Investors

While owner-occupiers are feeling the pinch, property investors face an entirely different set of mathematical challenges. Currently, the Bank of England base rate sits at 3.75%, held steady amid global geopolitical uncertainty and inflation fears.

For landlords, buy to let mortgage interest rates are typically higher than standard residential rates because lenders view investment properties as slightly higher risk. When reviewing the current buy to let mortgage rates, as of early 2026, the average two-year fixed rate sits at around 5.29%, while five-year fixes average 5.63% according to Moneyfacts.

This directly impacts how much an investor can borrow. Lenders require landlords to pass an Income Cover Ratio (ICR) stress test. They apply a "stressed" interest rate, usually between 5.5% and 6.0% to ensure the rental income easily covers the mortgage payments, even if rates rise further.

When market interest rates go up, this stress test becomes much harder to pass unless the rental income increases to match it. This requires investors to put down much larger cash deposits to buy a property today than they did a few years ago.

The Tax and Regulatory Squeeze

The pain of higher interest rates has been severely compounded for many individual, amateur landlords by two major factors:

- Section 24 Tax Changes: Fully implemented in 2020, Section 24 means individual landlords can no longer deduct their full mortgage interest from their rental income before paying tax. Instead, they are taxed on their total rental turnover and receive only a basic 20% tax credit. In a 5.5% interest rate environment, this can easily turn an otherwise profitable property into a loss-making one for higher-rate taxpayers.

- The Renters' Rights Act: Coming into force in May 2026, this legislation abolished Section 21 "no-fault" evictions, converted all tenancies into rolling contracts, and capped rent increases to once per year.

Squeezed by punitive taxes, increased regulatory burdens, and high borrowing costs, many amateur landlords have chosen to sell up and leave the market. Every region in the UK currently has fewer homes available to rent than it did before the pandemic.

What Does This Mean for Buy-to-Let Investors?

For sophisticated, well capitalised investors, the current environment may present an increasingly attractive long-term opportunity. The exit of the amateur landlord is reshaping the sector into a professionalised asset class.

What does this mean for those staying in the market?

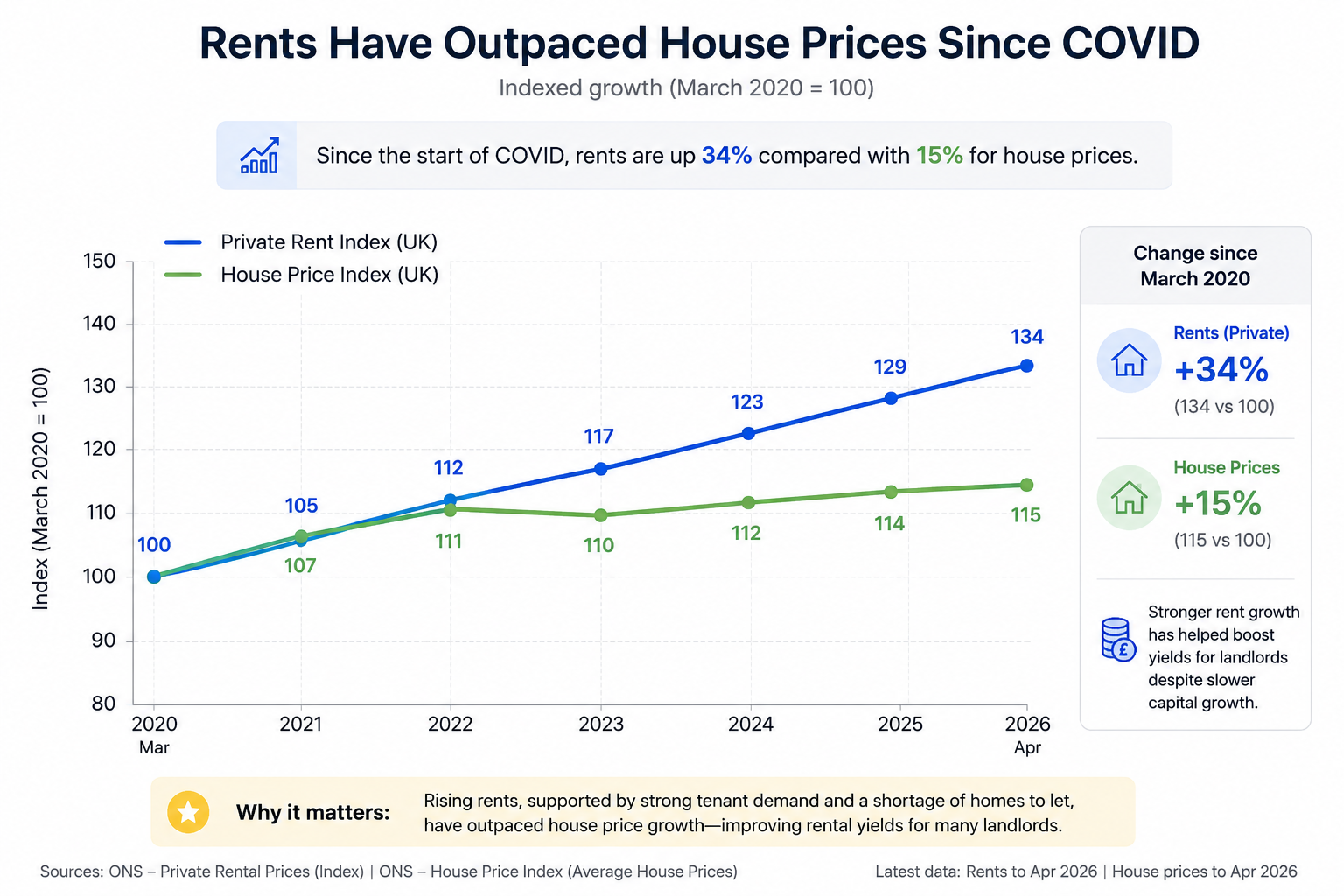

- Higher Yields Due to Rental Growth: Because the supply of rental homes has contracted sharply while tenant demand continues to grow, rents have surged. Recent data from Zoopla indicates that rents are rising by an average of 5% in lower cost regional markets - more than double the national rate of rental inflation. In many parts of the UK, rental growth has significantly outpaced house price growth since the pandemic, improving yields even as capital values have remained relatively subdued. The highest-yielding cities in the UK such as Sunderland, Aberdeen, and Burnley are currently offering average gross yields in excess of 8.0%.

Rents Have Outpaced House Prices Since the Pandemic

This dynamic supports the argument that rental yields have improved significantly despite slower capital appreciation.

- Less Competition from Amateur Landlords: With fewer casual investors competing for stock, professional investment platforms and portfolio builders face less competition when identifying and acquiring high-quality assets, granting them stronger negotiating power to secure favourable terms.

- More Motivated Vendors: The market currently features a higher proportion of motivated sellers, particularly retiring landlords looking to liquidate their portfolios to avoid the new Renters' Rights Act compliance burdens.

- The Rise of the Limited Company: To bypass the punitive effects of Section 24, the sector is rapidly professionalising. Properties held within Special Purpose Vehicles (SPVs) or Limited Companies remain exempt from Section 24, allowing landlords to offset 100% of their finance costs against Corporation Tax. This is why a record 66,587 buy-to-let companies were established in the UK in 2025.

For well capitalised investors with a long-term perspective, periods of uncertainty have historically created some of the best opportunities to acquire quality assets. The current market allows investors to lock in exceptionally high rental yields today, generating strong cash flow while they wait patiently for the macroeconomic environment to normalize and interest rates to fall.

What Happens if Rates Fall? The Uncoiling Effect

The core of the "coiled spring" thesis requires us to continually return to one central question: What happens if mortgage rates fall while wages remain elevated?

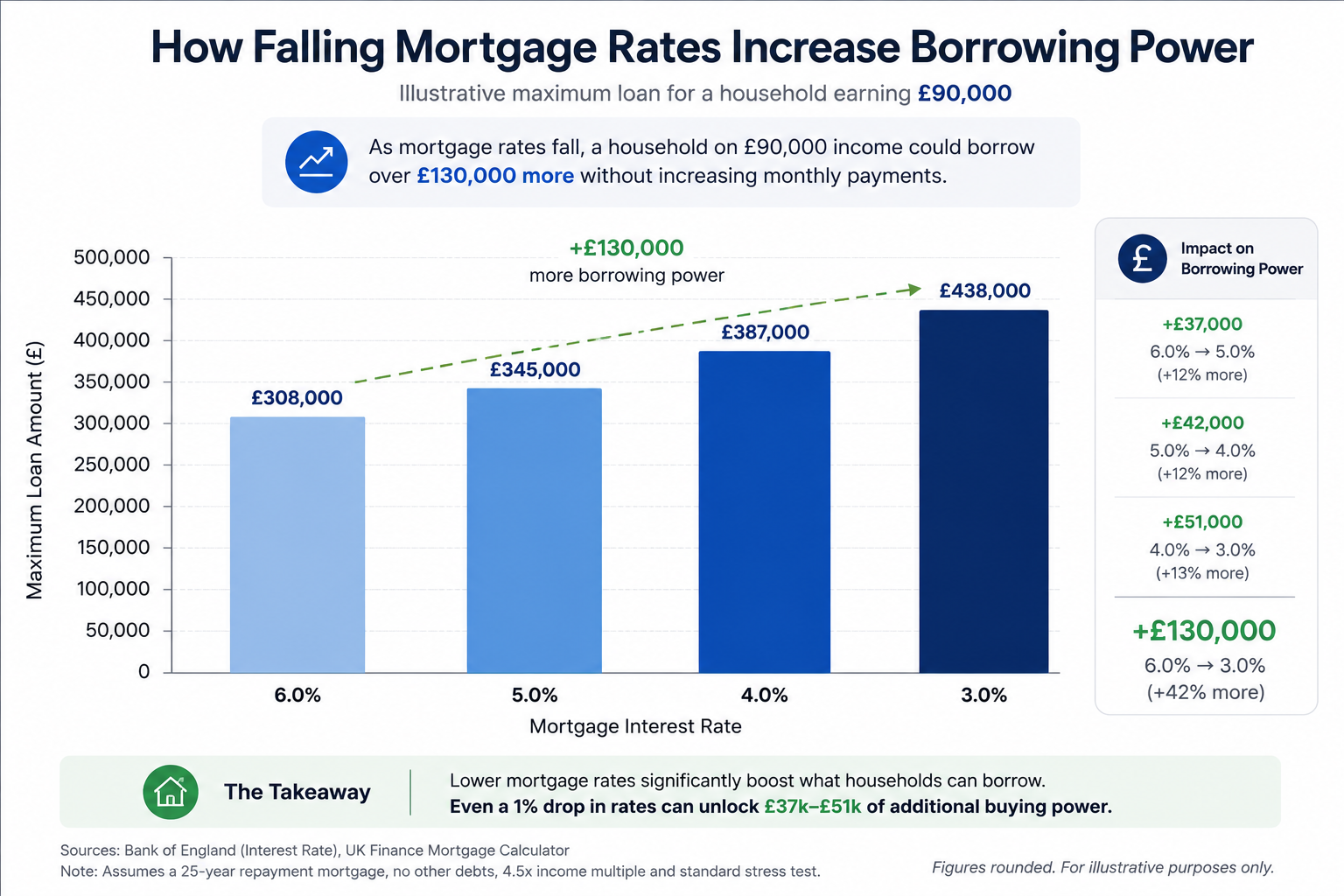

How Falling Rates Increase Borrowing Power

Based on a professional household earning £90,000, targeting a strict maximum monthly mortgage budget of £1,850 over a 30-year term.

If inflation settles and the Bank of England eventually cuts the base rate over the coming years, bringing standard mortgage rates down toward 3.5% or 4.0%, the monthly cost of borrowing will plummet. Suddenly, buyers will be able to pass lender affordability checks using their elevated post-COVID salaries.

This release of latent purchasing power, hitting a market with historically low levels of housing stock, could unlock latent demand and create significant upward pressure on house prices.

This aligns with broader expectations when examining any major house price forecast UK report. For instance, Savills forecasts average UK house prices will increase by 18.5% over the five years to 2030. The Office for Budget Responsibility (OBR) similarly forecasts steady, cumulative growth of 16.4% by 2031.

Downside Risks: What Could Keep the Spring Coiled?

While the coiled spring thesis is compelling, a thoughtful investor must always weigh the risks. Exploring scenarios where prices could fall is a necessary part of strategic portfolio planning.

The thesis depends heavily on interest rates eventually normalizing and labor markets remaining resilient. The main threats include:

- Higher for Longer Rates: If geopolitical tensions escalate, global energy and shipping costs could spike again. This would force the Bank of England to keep interest rates high to fight off a second wave of inflation, preventing any improvement in affordability.

- Recession and Rising Unemployment: The housing market's current resilience relies almost entirely on low unemployment and strong wage growth. If a deeper recession hits and unemployment spikes, that wage support evaporates. Forced sales would increase, driving property values down.

- Regulatory Pressures: Further tightening of landlord legislation or taxation could prompt an even larger sell-off of rental stock.

Some economists argue that improved affordability from wage growth may be offset by stricter lending regulation and structurally higher interest rates than the ultra-low-rate era of the 2010s. If mortgage rates settle permanently above historical norms, future house price growth may be more subdued than previous cycles.

While no market is without risk, current fundamentals suggest that severe nationwide price declines may be less likely than many fear.

Portfolio projection tool

Why Some Investors View Today's Market as an Opportunity

If the coiled spring thesis proves correct, today's market may present an unusually attractive environment for long-term investors.

Higher mortgage rates have reduced competition from owner-occupiers and less well-capitalised buyers, while transaction volumes remain below historical norms. In some areas, this has increased investors' ability to negotiate discounts and acquire assets on more favourable terms. Current market conditions may offer better entry points precisely because sentiment is weak, competition is lower, and long-term fundamentals remain supportive.

At the same time, rental demand remains strong, housing supply remains constrained, and wage growth is significantly higher than before the pandemic. This environment continues to deliver robust rental growth and improved yields for landlords capable of navigating the current debt landscape.

Of course, no investment opportunity is without risk. Interest rates may remain elevated for longer than expected, and broader economic conditions could deteriorate. However, periods of market uncertainty have historically created some of the best opportunities for investors willing to take a long-term view.

If mortgage rates eventually normalise while underlying fundamentals remain intact, future investors may look back on this period as one in which market pessimism created unusually attractive entry points.

The Verdict: A Market Waiting to Move

The UK property market in 2026 is navigating a complex transition. But looking past the immediate headlines of elevated mortgage rates reveals a market with surprisingly robust underlying fundamentals.

Post-COVID wages have fundamentally improved the financial carrying capacity of UK households. Chronic housing shortages continue to restrict the supply of physical homes. Rents are rising, and yields for professional investors are expanding rapidly.

Higher interest rates may be suppressing demand today, but stronger wages and limited supply continue to support long-term fundamentals.

The market may not be broken, it may simply be waiting for cheaper debt. If interest rates decline while incomes remain elevated, we could see a powerful uncoiling of latent demand.

For investors, the key lesson may not be to predict precisely when rates will fall, but to recognise that periods of uncertainty often create opportunities. Those able to acquire quality assets while competition is subdued may be well positioned if the housing market eventually begins to uncoil. Investors seeking to navigate this evolving market may benefit from a disciplined, long-term approach grounded in strong fundamentals.

-v1.avif)

Get investor insights and early access to opportunities

Join our investor briefings for structured insights, market updates, and priority access to new deals.

No spam, just timely insights for investors We respect your privacy and never sell your data

Case study

- Property Price:£275k

- Mkt Value at purchase:£290k

- Day one equity:£14,500

- Yield:7.2%

- ROCE:28.6%

.avif)