.jpg)

Will UK House Prices Crash in 2026?

In short a 2008 style housing crash appears unlikely. While higher interest rates and affordability pressures have slowed the market, structural housing shortages, stronger mortgage regulation and continued rental demand suggest a prolonged stagnation or localised correction is more likely than a systemic collapse.

Executive Summary

The UK housing market in 2026 is navigating a period of transition rather than crisis. While higher interest rates and affordability pressures have moderated activity, structural housing shortages, stronger mortgage regulation and resilient rental demand continue to support the market's long-term fundamentals. The following key findings summarise the primary drivers shaping UK house prices and property investment opportunities.

Key Takeaway

- A 2008-style UK housing crash appears unlikely given stronger mortgage regulation, widespread use of fixed-rate products, and significantly lower systemic leverage than previous downturns.

- Higher interest rates have materially reduced affordability, slowing transaction volumes and suppressing house price growth across many regions.

- While nominal house prices have remained relatively stable, inflation has caused a meaningful decline in real house prices since 2022.

- The UK continues to face a structural housing shortage, with long-term supply constraints providing support for residential property values.

- Cooling labour market conditions and weaker consumer confidence may contribute to localised corrections, though widespread forced selling remains unlikely.

- Regulatory changes, including the Renters' Rights Act, may further reduce rental supply, supporting rental growth and investor yields.

- For long-term investors, periods of market uncertainty can create opportunities to acquire assets below intrinsic value and benefit from future recovery cycles.

The UK macroeconomic environment in 2026 is undergoing a significant transition, shaped by geopolitical shifts, structurally higher interest rates, and notable legislative changes within the private rented sector. Following an energy shock linked to the conflict in the Middle East, the Bank of England has maintained a restrictive monetary stance. In its most recent policy decisions, the Monetary Policy Committee has held the base rate firm at 3.75%, signalling a clear departure from the low-interest-rate era of the previous decade. Consequently, the average two-year fixed mortgage rate has settled near 5.68%, representing a recalibration of debt costs for both retail homebuyers and property investors.

Against this complex macroeconomic backdrop, public discourse and mainstream media commentary frequently feature house price crash predictions. Daily headlines often conflate localised pricing adjustments with broader systemic risks. However, investors should focus on data rather than headlines when assessing the housing market. To answer the pressing question currently dominating the market, are house prices falling? - one must look beyond nominal headline figures. A rigorous assessment requires examining the underlying mechanics of housing supply, localised demographic demand, wage inflation, household debt structures, and the evolving regulatory landscape.

This comprehensive guide provides a data-driven analysis of the UK property market in mid-2026. It delineates the boundary between an orderly UK property downturn and a systemic market crash, evaluates the commercial impact of the Renters' Rights Act 2026, and explores why professional investors consistently utilise periods of perceived market vulnerability to acquire resilient assets. Throughout this analysis, Unity Property Investment maintains its commitment to remaining rational and data-driven during market cycles, providing investors with the clarity required to navigate periods of transition.

The Actual Reality: Are House Prices Falling?

To accurately determine whether the UK housing market is experiencing a structural depreciation, it is necessary to triangulate data across the primary indices. The market relies on figures published by the Office for National Statistics (ONS), alongside proprietary indices from major mortgage lenders such as Halifax and Nationwide. These institutions utilise different methodological frameworks, accounting for the slight divergence in their headline figures.

According to the comprehensive data provided by the ONS, the average house price for England stood at £290,000 in March 2026, representing a marginal year-on-year decline of 0.6%. In contrast, mortgage lender indices present a mixed picture. Halifax reported a 0.5% annual increase in UK house prices up to May 2026, despite a minor month-on-month contraction of 0.1%. Concurrently, Nationwide recorded an annual increase of 1.7%, noting a monthly decrease of 0.6% during the same period.

When these datasets are synthesised, the empirical reality becomes clear. While nominal price growth has broadly stalled at the national level, the market is not experiencing an uncontrolled decline. Instead, the UK housing market is navigating a prolonged plateau characterised by lower transaction volumes. Real-world asking prices are undergoing a necessary adjustment. The premiums that characterised the post-pandemic boom are being negotiated down by prospective buyers facing affordability constraints.

Crucially, the narrative of falling property prices is highly localised. Market performance is fragmented, dictated by regional affordability constraints, local economic health, and shifting demographic preferences. High-value markets with stretched price-to-earnings ratios are seeing corrections, while more affordable regions continue to demonstrate nominal growth.

This regional divergence underscores a critical reality for capital deployment. Capital-intensive markets such as Prime London are seeing values adjust as the cost of debt impacts multi-million-pound mortgages. Conversely, markets with lower entry points and stronger rental yields continue to demonstrate nominal capital resilience. Investors seeking reliable returns should align their investment criteria with areas backed by strong localised fundamentals. Detailed regional analysis and forward-looking metrics can be reviewed in our comprehensive UK House Price Forecast.

Defining the Downturn: The Mechanics of a Slowdown vs. a UK Housing Market Crash

Understanding the trajectory of the real estate sector requires precision in defining market movements. A UK housing market crash typically involves rapid, systemic declines in nominal asset values, accompanied by widespread negative equity, repossessions, and a collapse in banking liquidity. A housing market correction, by contrast, is an orderly recalibration where prices adjust downward either nominally or in real terms via inflationary erosion to restore historical affordability ratios without triggering a systemic financial crisis.

To grasp why the 2026 market is undergoing a controlled correction rather than a crash, it is helpful to examine the specific economic mechanics that drove historical downturns and contrast them with contemporary regulatory structures.

The 1989 Crash: The Interest Rate and Inflation Shock

The superficial trigger for the severe housing crash of 1989 was the withdrawal of MIRAS (Mortgage Interest Relief at Source) for unmarried couples. This policy shift prompted a surge in market demand as buyers rushed to complete purchases before the tax relief deadline expired. However, the underlying cause was the broader macroeconomic environment. Inflation was high, peaking at over 20% earlier in the decade, forcing the Bank of England to hike interest rates. By 1989, the base rate reached 15%. Because most mortgages were variable-rate products, this monetary tightening transmitted instantly to household balance sheets. Mortgage interest payments consumed a historic 27% of an average buyer’s gross income, leading to forced sales. The resulting oversupply caused prices to fall nominally by 19% over a 3.5-year period.

The 2008 Crash: The Global Liquidity Crisis

The 2008 Global Financial Crisis was a fundamentally different economic event. It was driven by the issuance of high-risk debt and the securitisation of toxic assets. The proliferation of subprime lending, 125% Loan-to-Value (LTV) mortgages, and self-certified loans created a housing market built on systemic risk. When the global credit markets froze, the supply of mortgage finance evaporated. Between mid-2007 and late 2008, UK house prices fell by approximately 16%. This crash was characterised by a severe liquidity drain, triggering negative equity and foreclosures.

The 2026 Market: Structural Resilience and Regulatory Safeguards

Current conditions differ significantly from previous housing crashes, making a 2008-style downturn less likely. The present landscape is defined by robust regulatory safeguards introduced by the Financial Conduct Authority (FCA).

Firstly, for over a decade, borrowers have been subjected to stress testing at interest rates higher than their initial mortgage pay rates. Secondly, unlike the variable-rate dominance of 1989, the majority of contemporary UK mortgages are fixed-rate products. While an estimated 1.8 million fixed-rate deals are scheduled for renewal in 2026, borrowers have had lead time to adjust spending or negotiate extended mortgage terms. Thirdly, due to sustained capital appreciation over the last decade, the aggregate LTV ratio of the UK housing stock is low. Negative equity remains statistically insignificant across the broader market.

Therefore, the current scenario is best classified as a low-transaction slowdown. Transaction volumes have dropped with Q1 2026 completions falling to 269,000, roughly 30,000 below the five-year average, as buyers and sellers remain locked in a pricing stalemate. This resulting gridlock is a hallmark of a housing market correction.

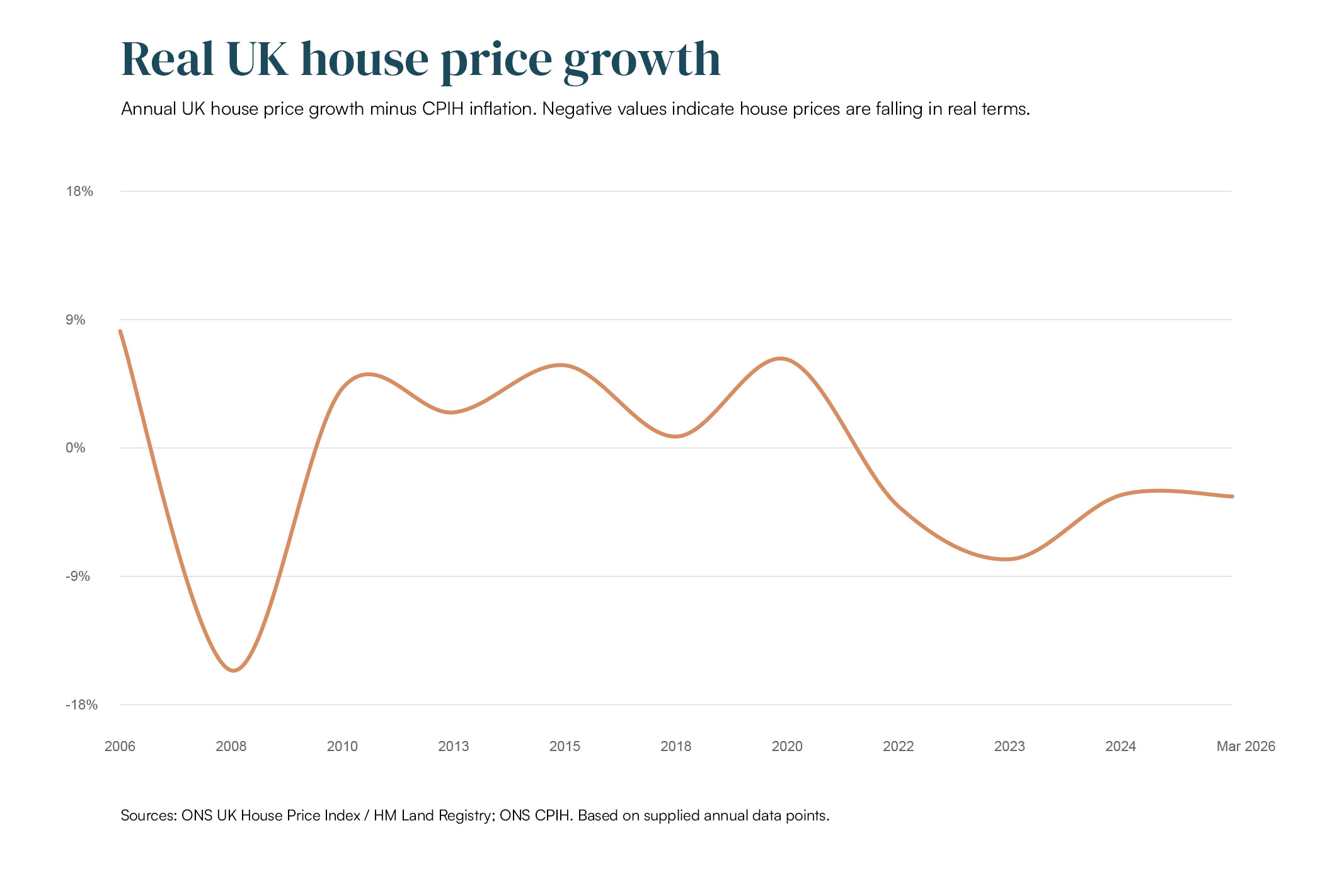

Figure 1: Real UK House Price Growth (2006–2026)

Since 2022, inflation has outpaced nominal house price growth, resulting in a meaningful real-term correction despite the absence of a 2008-style housing crash.

This dynamic - stagnant capital values coupled with rising rental incomes, leads to yield expansion, making the underlying asset fundamentally more cash-generative.

Cash-flow positive assets allow the investor to hold the property and wait for the macroeconomic cycle to rotate.

Macroeconomic Headwinds: Interest Rates, Affordability, and the Bank of England

To project the trajectory of property values, one must analyse the cost of capital. In its highly anticipated April 2026 meeting, the Bank of England’s Monetary Policy Committee (MPC) voted 8–1 to hold the Base Rate at 3.75%. The sole dissenting vote favoured an immediate hike to 4.0%, underscoring a hawkish posture within the Bank.

The persistence of this restrictive monetary environment is influenced by geopolitical shocks. The conflict in the Middle East has disrupted energy supply chains, impacting shipping routes and wholesale oil markets. As a result, Consumer Prices Index (CPI) inflation rose to 3.3% in March 2026. The Bank anticipates that inflation will remain elevated through the third quarter as indirect economic effects permeate the economy. Consequently, market expectations for rapid interest rate cuts in 2026 have shifted toward a "higher for longer" environment.

This macroeconomic reality dictates retail mortgage pricing. Two-year fixed mortgage rates average 5.68% as of mid-2026, while five-year fixes hover around similar levels.

For the prospective homeowner or retail buy-to-let investor, this represents a notable affordability ceiling. A mere 0.50 percentage point increase in the base rate adds approximately £906 per year to the repayments on a standard £250,000 mortgage. Equifax data indicates that aggregate mortgage repayments across the UK remain 45% above January 2022 levels, with 11% of all new mortgage originations now stretching beyond 35-year terms.

Professional investors track these metrics meticulously via our analysis on buy-to-let interest rates to optimise their capital leverage strategies. While structurally high rates act as a headwind for the highly leveraged retail buyer, they push prospective first-time buyers back into the rental sector, thereby driving up tenant demand.

Interested in building a resilient property portfolio? Explore our investment areas and portfolio tools.

The Misery Index: The Role of Inflation, Wage Growth, and Unemployment

Asset prices are intrinsically linked to the health of the broader labour market. A central risk to the stability of the housing market is the potential for rising unemployment to trigger forced sales.

Data released by the ONS for the first quarter of 2026 reveals a cooling labour market. The headline unemployment rate rose to 5.0%, marking its highest level since 2015, while youth unemployment (ages 16-24) reached 16.2%. The number of payrolled employees contracted by 104,000 between March 2025 and March 2026. Correspondingly, job vacancies fell to a five-year low of 705,000, signalling a deterioration in corporate hiring appetite.

Nominal regular earnings growth has slowed to 3.4%. When adjusted for the cost of living, real wage growth stands at just 0.1%. This combination of rising inflation and rising unemployment poses a challenge to domestic demand, limiting the capacity of the general population to service outsized mortgage debts.

However, the nuance required to understand the current market lies in recognising how this housing market is correcting. When nominal house prices remain flat for a multi-year period while consumer price inflation runs concurrently at 3% to 4%, the inflation-adjusted value of the property is falling. This phenomenon, inflationary erosion is currently facilitating a quiet housing market weakness. The physical asset is depreciating in real economic terms without experiencing a nominal crash.

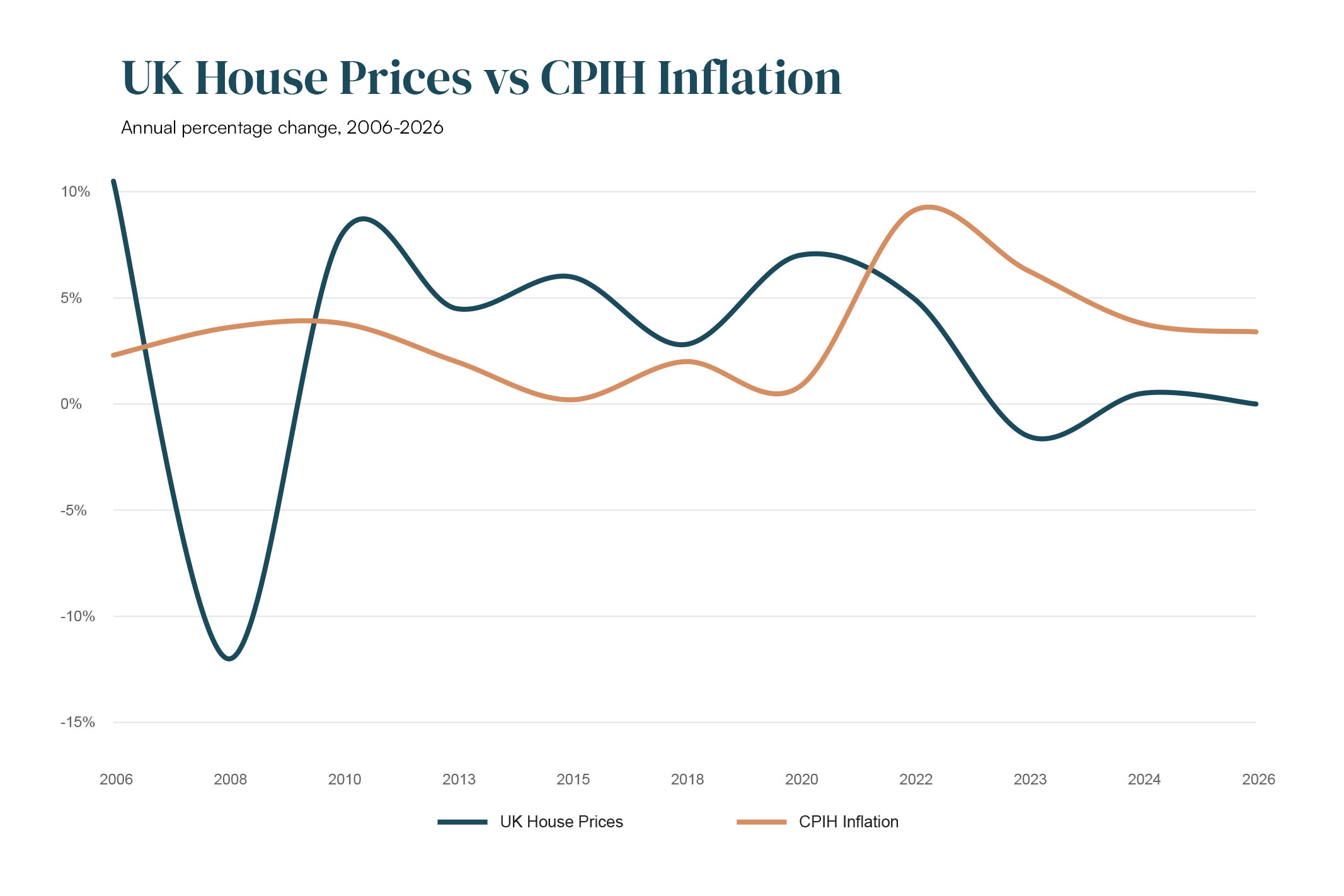

Figure 2. UK House Prices vs CPIH Inflation (2006–2026)

Simultaneously, persistent inflation erodes the real value of an investor’s long-term fixed-rate mortgage debt, underscoring why tangible property remains a proven inflation hedge.

Regulatory Pressures: The Renters' Rights Act 2026 and Strategic Landlord Exits

The UK property market is currently undergoing significant legislative restructuring. The Renters' Rights Act 2026, which came into force on May 1, 2026, has altered the operational mechanics and compliance requirements of the Private Rented Sector (PRS).

The legislation has introduced reforms that mandate operational changes for landlords:

- Abolition of Section 21: The elimination of "no-fault" evictions means landlords can no longer repossess properties without citing a legally valid ground.

- End of Fixed-Term Tenancies: Private rented sector tenancies have transitioned into assured periodic (rolling) tenancies. Tenants can leave with two months' notice, transferring void risk onto the landlord.

- Rent Control Mechanisms: Rent increases are limited to once per year and must be executed via a statutory Section 8 notice. Tenants possess the right to challenge any rent increase at a First-tier Tribunal.

- Additional Compliance Burdens: The Act introduces bans on rental bidding, new statutory rights regarding pets, and paves the way for the integration of Awaab’s Law. Non-compliance carries civil penalties of up to £40,000.

The financial impact of these regulations on amateur landlords has been notable. A government-linked survey indicated that 31% of landlords intend to reduce their portfolios, and 16% plan to exit the market by the end of 2026. The National Residential Landlords Association (NRLA) reported that 26% of landlords sold properties in late 2024.

Many smaller landlords are exiting the market, creating opportunities for better-capitalised investors seeking UK property investment opportunities. When a landlord sells a property, it transitions from the PRS to the owner-occupier market, but the structural supply-demand imbalance of the nation remains unchanged.

As retail landlords list tenanted or unmodernised properties at a discount to secure a fast sale, professional asset management firms acquire these assets. This transfer of housing stock to institutional-grade management stabilises the broader market while creating entry points for strategic capital. For assistance in navigating these legislative shifts, Unity offers dedicated property management services designed to shield investors from compliance friction.

Market Resilience: Why Sensational Headlines Exaggerate Market Fear

Financial media frequently frames minor drops in average house prices as the vanguard of a broader collapse. However, these headlines often ignore the most potent force supporting UK property values: the chronic, structural deficit of physical housing supply.

Despite various government housing targets, the UK has chronically failed to build the 300,000 homes per year necessary to meet demographic expansion. While housing starts saw a temporary uptick in late 2025, the aggregate housing deficit remains substantial. High commercial borrowing costs and material inflation have caused housebuilders to scale back their construction pipelines for 2026 and 2027.

This supply shortage places a rigid floor under property prices. Even when buyer demand falls due to higher mortgage rates, the lack of available inventory prevents prices from entering a freefall. Homeowners, shielded by long-term fixed mortgages and substantial equity buffers, often choose to stay put, reducing the supply of homes for sale. This is the primary reason why transaction volumes fall before prices do.

Simultaneously, the UK population continues to grow. With purchasing power restricted, this pent-up demand is funnelled into the rental sector. Consequently, while nominal house prices remain flat, average UK private rents surged by 3.5% to a record £1,381 in the 12 months to April 2026.

This dynamic, stagnant capital values coupled with rising rental incomes, leads to yield expansion, making the underlying asset fundamentally more cash-generative.

Regional Divergence: Prime London vs. The Expanding Commuter Belt

A nuanced understanding of the 2026 real estate market requires abandoning the idea of a uniform national trend. The UK market is fracturing along regional lines.

The Stagnation of Prime London

London is demonstrating weaker performance, with prices falling 2.1% annually to an average of £542,000. London's market dynamics are highly correlated with interest rates because the absolute debt levels required are immense. Prime London rental yields are also notoriously low, providing little cash-flow buffer for leveraged investors.

Conversely, regions such as the East Midlands registered a 0.7% annual price rise, supported by a more realistic price-to-earnings ratio. In regions where average house prices sit closer to £215,000 to £250,000, mortgage rates are painful but not prohibitive. Gross yields in these robust northern and midlands regions can exceed 7%, offering operational cash-flow dynamics that insulate the investor against short-term capital volatility.

The Commuter Belt Freehold Resilience

One of the most structurally secure trends has been the expansion of the commuter belt. Post-pandemic hybrid working paradigms have altered geographical demand. The commuter sweet spot has expanded into a 60-to-90-minute radius, encompassing previously overlooked areas in the broader South East.

Within these zones, asset selection is the defining factor. Retail investors are frequently lured into high-density new build apartments, which often carry a "New Build Premium" of 10% to 20% over established local stock. In a correcting market, this premium can evaporate, leaving the investor in negative equity, while service charges suppress long-term capital growth.

Professional investment firms focus on standard, 2-to-3 bedroom freehold houses within rail-connected commuter towns. Freehold houses appeal to a broader demographic, ensuring high tenant retention and resale liquidity. Quality freehold commuter-belt stock remains resilient during economic downturns.

Professional Strategy: Why Sophisticated Investors Buy During Uncertainty

Periods of uncertainty can create attractive opportunities for long-term investors. In the rational market of 2026, the power dynamic has shifted toward buyers. Motivated sellers, whether exiting landlords or homeowners navigating higher fixed-rate mortgages are receptive to negotiation.

The Defensive Power of Cash-Flow Positive Property

The key to navigating a market correction is operational cash flow. If a property portfolio generates sufficient rental income to cover elevated mortgage interest costs and management fees whilst delivering a net positive return, short-term fluctuations in capital value are less relevant. Cash-flow positive assets allow the investor to hold the property and wait for the macroeconomic cycle to rotate. Professional buyers rely heavily on rigorous due diligence before acquiring an asset.

Want to stress-test your portfolio against different interest rate scenarios? Use our buy-to-let calculator.

The BRRR Strategy and Forced Capital Appreciation

Rather than relying on passive capital growth, sophisticated investors utilise active asset management. For investors exploring value-add opportunities, the BRRR strategy (Buy, Refurbish, Refinance, Rent, Repeat) remains highly effective in the current market in right areas for those with a long term investment timeframe.

This strategy targets unmodernised housing stock, often lagging below the Energy Performance Certificate (EPC) 'C' standard. Capital is injected to execute energy retrofits and modernisations, forcing immediate capital appreciation. The newly modernised asset is then refinanced at the elevated commercial valuation.

This methodology turns a macroeconomic headwind into an operational advantage. By forcing value into the asset, the investor creates an equity buffer. To understand the operational logistics required to execute this strategy, review our process on how we source properties and view real-world examples in our case studies.

Portfolio projection tool

Core Risks to Watch in 2026 and Beyond

Current conditions differ significantly from previous housing crashes, making a 2008-style downturn less likely. However, objective monitoring of economic indicators remains essential.

- Unemployment Contagion: If corporate distress deepens due to the global energy shock, a sudden spike in broad-based unemployment could compromise the ability of homeowners to service their mortgages.

- Rates Staying Structurally Higher for Longer: If geopolitical instability continues, the Bank will be compelled to hold the base rate near 4.0% to combat imported inflation, suppressing transaction volumes and compressing purchasing power.

- Tighter Commercial Lending Criteria: Commercial banks may proactively tighten risk parameters. A severe contraction in credit availability would impact the lower end of the market, affecting the pipeline of first-time buyers.

- Further Regulatory Creep: Future phases of the Renters' Rights Act, including Awaab’s Law and the Decent Homes Standard, will necessitate further capital expenditure from landlords. Investors must ensure their assets are future proofed and energy efficient.

Navigating these risks requires professional oversight. Engaging with experienced property investment consultants allows capital to be deployed systematically, hedging against macroeconomic risk.

Conclusion: The Supremacy of Long-Term Compounding Over Short-Term Sentiment

The long term fundamentals of UK housing remain supported by structural supply shortages. The empirical data indicates that the market is undergoing a measured, orderly, and highly localised correction. Elevated interest rates and inflationary pressures have reset affordability boundaries, naturally suppressing nominal price growth. Concurrently, the legislative overhaul represented by the Renters' Rights Act is shifting the dynamics of the private rented sector.

However, beneath the headline-driven surface, the core fundamentals of UK real estate remain strong. The nation experiences an ongoing shortage of physical housing, while population growth and household formation continue. Consequently, tenant demand is driving rental yields to attractive levels. The lack of retail competition allows for negotiation and the strategic acquisition of high-yielding commuter-belt freeholds.

Real estate is a robust mechanism for wealth preservation and compounding economic growth. The superior strategy is to acquire tangible assets that cash-flow positively and hold those assets securely through the macroeconomic cycle.

Unity Property Investment acts as an analytical, data-driven partner throughout market cycles. By combining macroeconomic analysis, rigorous due diligence, and disciplined asset selection, we help investors build resilient portfolios designed for long-term wealth creation. To understand how we operationalise these principles, explore our about page. For a personalised assessment of your strategy, utilise our portfolio projection tools or book a consultation with our advisory team to discuss how a disciplined investment approach can help navigate changing market conditions.

Frequently Asked Questions (FAQ)

Will UK house prices crash in 2026?

A systemic crash like 2008 remains unlikely. The current market is experiencing a prolonged stagnation and a localised correction due to higher borrowing costs, but strict mortgage stress testing and low negative equity levels prevent a collapse.

Are UK house prices falling?

Nominally, UK house prices are plateauing, with slight regional variations. For example, in early 2026, London saw a 2.1% annual contraction, while Wales and Northern Ireland saw increases of 2.9% and 7.4% respectively. In real terms (adjusted for inflation), values have eroded more significantly.

What happens to buy-to-let during a recession?

During economic downturns, first-time buyers are often priced out of the purchase market, which increases demand for rental properties. Consequently, high-quality, fairly priced rental stock usually experiences low void periods and rising yields.

Is now a good time to invest in property?

Periods of uncertainty can create attractive entry points. With amateur landlords exiting the market and transaction volumes low, professional investors have stronger negotiating power to acquire below-market-value properties and execute forced-appreciation strategies.

Which UK regions are most resilient?

High-yielding commuter belt areas (60-90 minutes from London), the North West, and the East Midlands are demonstrating strong resilience. They offer better affordability, high tenant demand, and gross yields that can comfortably absorb higher mortgage costs.

Will interest rates cause house prices to fall?

High interest rates cap purchasing power, which suppresses the prices buyers can afford to pay. This has caused a stagnation in nominal house price growth and a drop in transaction volumes, but chronic housing shortages place a floor under how far prices can fall.

What happened during the 2008 housing crash?

The 2008 crash was driven by a global liquidity crisis and the collapse of subprime, highly leveraged mortgages. Credit froze entirely, and UK house prices plummeted by approximately 16% over 18 months, leading to widespread negative equity and bank foreclosures.

Could the Renters' Rights Act reduce housing supply?

While the Act has prompted approximately 26% of surveyed landlords to sell properties, this shifts stock from the rental market to the owner-occupier market. The physical supply of homes remains the same, though it is triggering a transfer of assets from amateur to professional, institutional-grade investors.

Comparative Analysis of Historical UK Property Crashes vs Current Market Dynamics

Economic Metric

1989-1992 Market Crash

2008-2009 Financial Crisis

2026 Market Conditions

.png)

-v1.avif)

Get investor insights and early access to opportunities

Join our investor briefings for structured insights, market updates, and priority access to new deals.

No spam, just timely insights for investors We respect your privacy and never sell your data

Buy to let investment and rental yield calculator

Regional UK House Price Variations and Market Dynamics (March 2026)

Region / Nation

Average Property Price

Annual Change (%)

Underlying Market Dynamics and Investor Context

Case study

- Property Price:£275k

- Mkt Value at purchase:£290k

- Day one equity:£14,500

- Yield:7.2%

- ROCE:28.6%

.avif)